History & recent developments

NewConnect was launched on 30 August 2007 as an alternative market of the Warsaw Stock Exchange for young, innovative companies with high growth potential. From the start, it was intended to offer young companies an easy and inexpensive way to become publicly traded. In its early years, the NewConnect segment grew rapidly — in a record-breaking 2011, 172 companies made their debut. After several scandals that caused significant losses for investors, the market is currently undergoing revitalization, including segmentation such as NC Focus for high-quality companies and simplification of information procedures.

Sources: Google search, East Value Research

Current market statistics

Currently, the website www.newconnect.pl lists 356 companies from various sectors, thereof 5 foreign ones. Their total market capitalisation equals PLN 13.3bn. On December 9, trading turnover equalled PLN 5m/EUR 1.18m, with Sygnis S.A. (PLN 467k, Sector: Additive production technologies), Scanway S.A. (PLN 381k, Sector: Space) and Grupa Niewiadow-PGM (PLN 401k, Sector: Defense) being the most traded stocks. In Q3/25, the total trading turnover amounted to PLN 672.7m/EUR 159m.

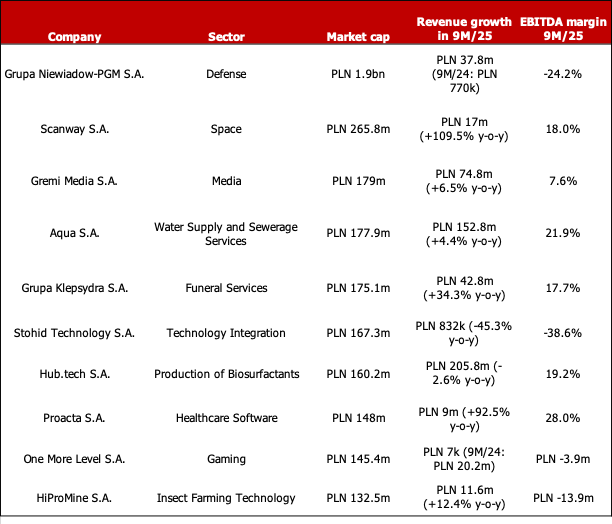

Below is a list of the 10 largest NewConnect companies by market cap:

Sources: stooq.pl, bankier.pl, company websites, East Value Research GmbH

Success stories and controversies

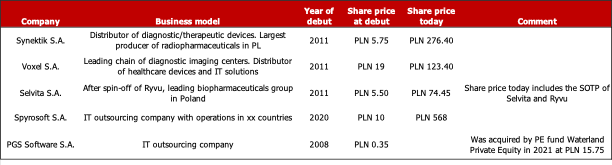

There are a number of companies that debuted on the NewConnect segment—often to raise equity capital for growth because the VC sector is underdeveloped in Poland—over the years grew their business and valuation significantly, and finally moved to the regulated main market of the Warsaw Stock Exchange. Examples include Synektik S.A., a distributor of diagnostic and therapeutic devices and producer of radiopharmaceuticals; Voxel S.A., the leading operator of diagnostic imaging centers in Poland and distributor of medical devices and IT solutions; Spyrosoft S.A., an IT outsourcing company with operations in 10 countries on 4 continents; Selvita S.A., which today — after the spin-off of Ryvu Therapeutics — is the leading Polish biotechnology group; and PGS Software S.A., another IT outsourcing company, which in 2021 was aquired by a Dutch private equity group.

Sources: Google search, East Value Research GmbH

On the other hand, there are also multiple examples of NewConnect-listed companies that do not meet basic corporate governance standards, delay the release of financial reports, and have very low daily trading volume, which makes it difficult to buy or sell larger positions. In recent years, the Warsaw Stock Exchange has put stronger focus on eliminating these pathologies.

Recommendation for investors

Although they can generate significant returns for shareholders, we believe that investments in the NewConnect segment require a very profound due diligence of the company’s business models, their management teams and shareholders. We recommend to commit only a small fraction of the portfolio value to these companies.

Author: Adrian Kowollik