This blog post marks the beginning of a series of analyses focused on Polish companies and their listed direct German counterparts.

In this installment, we will delve into the examination of Oponeo.pl S.A., a company listed on the main market of the Warsaw Stock Exchange since 2007, and Delticom AG, headquartered in Hannover. Delticom AG holds the position of a European leader and has been listed on the Frankfurt Stock Exchange since 2006.

History & current business

Oponeo.pl was founded in 1999 by university friends Dariusz Topolewski and Ryszard Zawieruszynski, who continue to own and manage the company today. It is headquartered in Bydgoszcz, Poland. Over the years, the company has grown to become the largest online retailer of tires and rims in Poland, holding a market share of over 75%. In recent years, Oponeo has expanded its operations to 12 foreign markets, primarily in EU countries but also in Turkey. The company has successfully established or acquired other e-commerce businesses, including Dadelo, an online shop for bikes and sports accessories that is also listed on the Warsaw Stock Exchange, and Rotopino.pl, an online retailer of tools. Oponeo Group currently operates 25 online shops, employs 348 individuals, and owns a modern, automated warehouse in Poland spanning 72,000 square meters. Additionally, Oponeo has formed partnerships with over 1,000 fitting service providers in Poland and more than 3,000 in its other markets. The company relies on wholesalers and producers for distribution to foreign clients.

Delticom, also founded in 1999, has become the largest online retailer of tires and rims not only in Germany but also across Europe. While Delticom faces strong competition from Oponeo in countries like the Netherlands and Belgium, it held a presence in the United States until 2022, when Delticom North America was sold (the transaction generated a one-off gain of EUR 3.8m). In 2016, Delticom’s founders, Andreas Prüfer, Rainer Binder, Philip von Grolman, and Timon Samusch, attempted to diversify their business by acquiring an online distributor of used cars in France and online shops for gourmet and regular food in Germany. However, due to liquidity issues, these diversification efforts were ultimately discontinued in 2019-2020. Presently, Delticom has refocused its efforts on its core activity of selling tires and rims. The company operates approximately 300 online shops in nearly 50 countries, employing 168 individuals. Delticom runs warehouses in Sehnde, Germany (over 60,000 square meters), and Ensisheim, France (around 50,000 square meters).

Historical & current financials

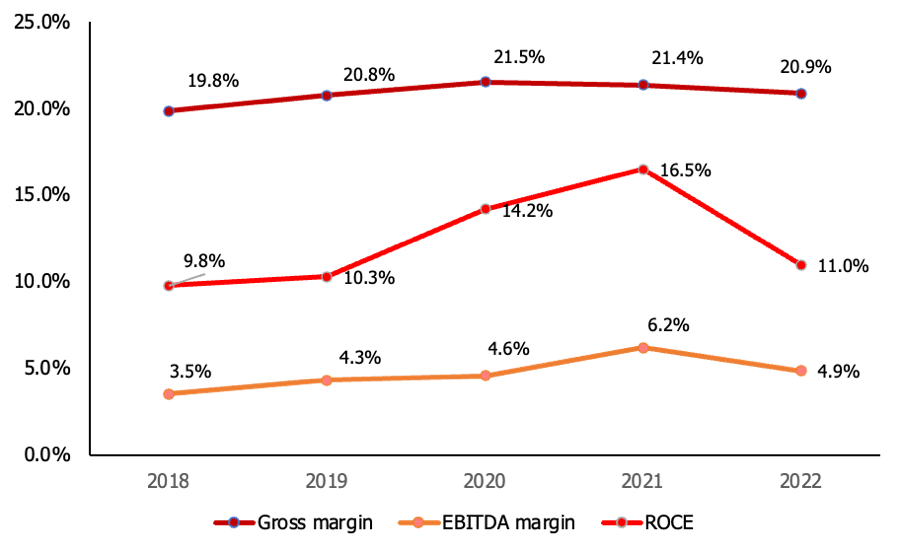

Oponeo boasts an impressive track record when it comes to its financial performance. Between 2012 and 2022, the company managed to increase its revenues from PLN 207.1m to PLN 1.7bn, achieving a CAGR of 23.4%. Concurrently, its EBITDA also saw a substantial rise, climbing from PLN 6.7m to PLN 82.5m (CAGR of 28.5%). Over the past five years, Oponeo has maintained EBITDA and ROCE figures within the range of 3.5% to 6.2% and 9.8% to 16.5%, respectively.

Since 2008, Oponeo has consistently been distributing dividends to its shareholders and has also regularly engaged in stock buyback initiatives. Despite the challenging situation prevailing in the retail sector at present, the company displayed notable resilience. In the first half of 2023 (H1/23), Oponeo achieved a year-on-year revenue growth of 14.1%, amounting to PLN 789.4m. However, there was a decline of 9.6% in EBITDA, reaching PLN 18.9m during the same period. The company has managed to maintain a reasonably low net gearing level of 11.3%.

Oponeo.pl S.A.: Gross & EBITDA margins and ROCE in 2018-2022

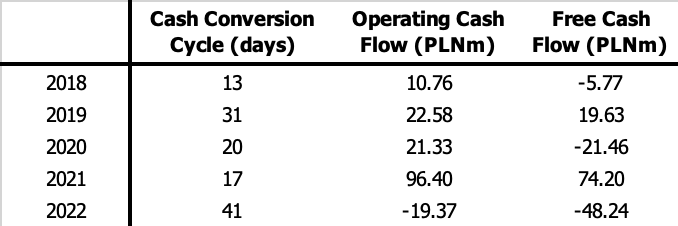

Oponeo.pl S.A.: Cash Conversion Cycle, Operating and Free Cash Flow in 2018-2022

Source: Company information, East Value Research GmbH

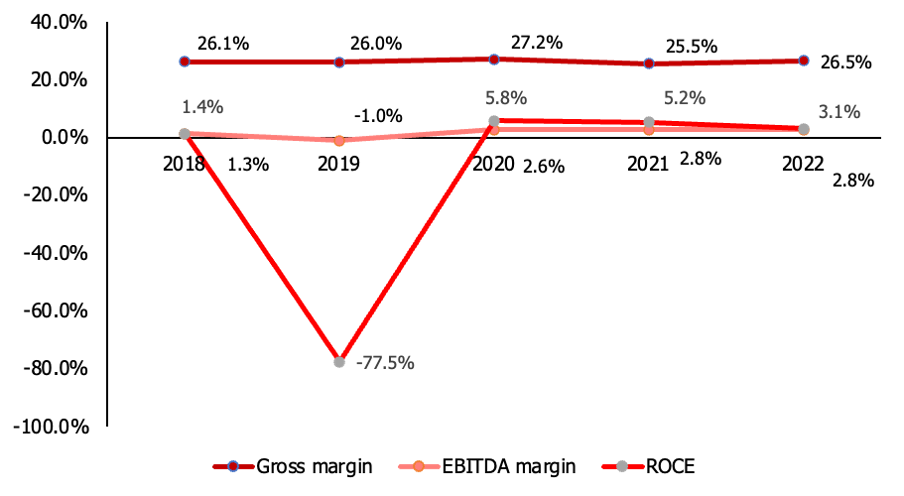

An examination of Delticom’s historical performance presents a mixed overview. Between 2012 and 2018, the company experienced a consistent growth in sales, averaging a 6.5% increase annually, accompanied by a clearly positive EBITDA margin. However, due to an unsuccessful expansion into the online food business, the company’s profitability suffered a steep decline in 2019. During that year, Delticom reported an EBITDA of EUR -6.6m and an EBIT of EUR -42.1m. Consequently, the company’s net debt escalated to EUR 87.8m, causing a substantial drop in Delticom’s share price from its peak of around EUR 80 in 2011 to below EUR 3.

Nonetheless, following a restructuring effort, the company managed to restore a positive operating profit trajectory. Presently, Delticom is poised to achieve an estimated EBITDA of approximately EUR 14m this year. In the first half of 2023, the company’s revenues experienced a year-on-year decline of 10%, amounting to EUR 197.7m. This contraction was primarily attributed to a redirection of revenues towards Delticom’s newly established marketplace, Reifen.com. Within this platform, the company sells car accessories from third-party retailers, earning commissions.

The net gearing ratio stood at 200.5%, but this included an estimated EUR 50m of IFRS 16 related leasing debt, thus the actual net debt figure was not EUR 82.8m but EUR 32.8m (equity equalled EUR 41.3m). At the end of 2021 and 2022, the respective net gearing amounted to 138.5% and 178% respectively. In H1/23, the increase was driven by the accumulation of inventories in preparation for the crucial winter season, a common practice in Delticom’s sector. However, it is anticipated that by the end of 2023, the net gearing ratio will once again substantially decrease compared to the value recorded as of June 30, 2023.

Delticom AG: Gross & EBITDA margins and ROCE in 2018-2022

Source: Company information, East Value Research GmbH

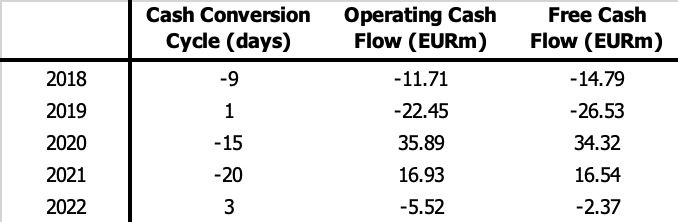

Delticom AG: Cash Conversion Cycle, Operating and Free Cash Flow in 2018-2022

Source: Company information, East Value Research GmbH

Current valuation & conclusion

Compared to Delticom, Oponeo has a more favorable track record, and we possess greater confidence in its management. Nevertheless, we believe that much of this positivity is already factored into the company’s current valuation metrics. For instance, Oponeo’s estimated enterprise value to sales ratio (EV/Sales) for 2023E is 0.3x, which is in line with the 5-year average of 0.4x. Similarly, its EV/EBITDA ratio for 2023E is 7.7x compared to the 5-year average of 6.7x.

On the other hand, Delticom presents an intriguing restructuring narrative, particularly due to its current historically low valuation. The projected EV/Sales ratio for 2023E is 0.2x, consistent with the 5-year average. Likewise, the projected EV/EBITDA ratio for 2023E is 6.9x as opposed to the 5-year average of 9.9x. Notably, Delticom exhibits a notably higher revenue per employee compared to Oponeo, amounting to EUR 1.18m versus EUR 507.5k.

Assuming that inflationary pressures ease, which we anticipate occurring in Q4/23E, and if online sales rebound, Delticom’s financial performance and market valuation are likely to follow suit. A scenario reminiscent of 2020-21 could emerge, wherein Delticom experienced a significant improvement in EBITDA compared to 2019, leading to a substantial increase in its stock price. During the period between mid-2020 and mid-2021, the stock price surged from a low of approximately EUR 2.50 to EUR 9.70. Although we believe the potential return currently exceeds 100%, it’s important to acknowledge key risks such as elevated net gearing and concerns surrounding Delticom’s founder and CEO, a figure who generates controversy among institutional investors. Nevertheless, we hold the view that the company’s prevailing trading multiples already adequately account for these factors.