A troubled history The Balkan countries had a much more difficult post-communist transition than other CEE countries. The breakup of Yugoslavia and the ensuing Yugoslav wars completely destroyed the trade infrastructure, with foreign direct investments completely bypassing the region and flowing to other Eastern European countries instead. The history has caused an economic impact still […]

Business description Rex Concepts was established in 2022 by Olgierd Danielewicz and Peter Kaineder, both of whom previously held senior management roles at AmRest, the largest quick-service restaurant chain (QSR) operator in Central and Eastern Europe. They partnered with experienced food investor McWin and secured an exclusive regional master franchise agreement with Restaurant Brands International […]

To access this post, you must have one of the following subscriptions: Annual Plan.

In 1990, Romania had a GDP per capita similar to Poland’s. Today, it is more than ten years behind its CEE peer in terms of development, which in our view mainly results from weak governance and populist fiscal policies. Nevertheless, we are convinced that the EU country – and especially its listed companies – offer […]

Business description Since 1995, when its predecessor Excalibur Army was founded by Mr. Jaroslav Strnad—the father of its current CEO and owner—the Czechoslovak Group (CSG) has grown organically and through acquisitions into a global operation with more than 100 subsidiaries and over 14,000 employees. Today, the Group, which is based in Prague, is a rapidly […]

To access this post, you must have one of the following subscriptions: Annual Plan.

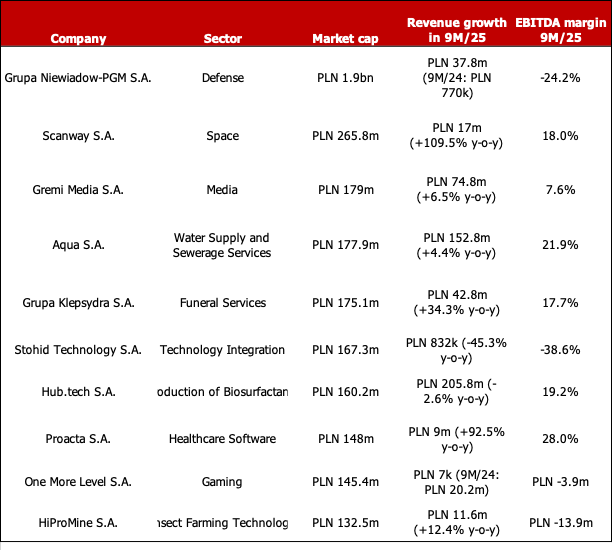

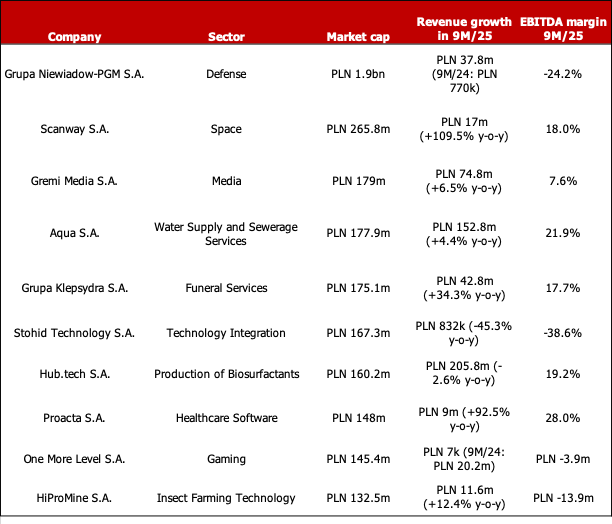

History & recent developments NewConnect was launched on 30 August 2007 as an alternative market of the Warsaw Stock Exchange for young, innovative companies with high growth potential. From the start, it was intended to offer young companies an easy and inexpensive way to become publicly traded. In its early years, the NewConnect segment grew […]

Business summary Owned by three members of its management board, who still control >50% of the votes, Wirtualna Polska Holding (WPL) is the largest Polish operator of online portals. Among its websites, there are wp.pl and o2.pl, the 2nd and 4th most popular online information portals in Poland, money.pl (No 1 financial portal in Poland), WP […]

To access this post, you must have one of the following subscriptions: Annual Plan.