On November 5, the scenario many Western European politicians had feared became a reality: Donald Trump won the U.S. presidential election by a significant margin, securing 312 electoral votes to Kamala Harris’s 226.

If Trump follows through on the promises he made during his campaign — and based on his actions during his first four years in office, we believe he will — times could become difficult for Europe. Two of his main objectives are the widespread use of tariffs on both Chinese and European goods to support American industry, and the immediate end of the Russia-Ukraine war, where the U.S. has so far been Ukraine’s largest supporter.

Trump’s economic policy — e.g. there are discussions about a min. 10% tariff on European and a 60% tariff on Chinese products https://www.reuters.com/world/europe-will-pay-big-price-trump-warns-tariffs-2024-10-30/ — would make European goods significantly more expensive for US consumers and thus reduce Europe’s competitiveness. It’s worth noting that the U.S. is currently among the top three trading partners for many EU member states, including Germany and France (Source: destatis, World Bank, Google search) and the largest partner for the whole EU https://ec.europa.eu/eurostat/statistics-explained/index.php?title=File:Principal_partners_for_EU_exports_of_goods,_2023.png Furthermore, Trump could pressure the EU to choose between aligning with the US in its policy against China or maintaining its current business relationship with the Asian country, which is the bloc’s 3rd largest trading partner. This would be a particularly bad scenario for German car manufacturers, which generate between 16.1% (BMW) and 23.3% (Porsche) of their yearly revenues in China.

In terms of geopolitics, Trump aims to keep the U.S. out of foreign conflicts that cost American taxpayers billions. He also insists that all NATO countries spend at least 2% of their annual GDP on defence. During his first term as president, he even threatened that the US — by far the bloc’s largest financial contributor — could withdraw from NATO.

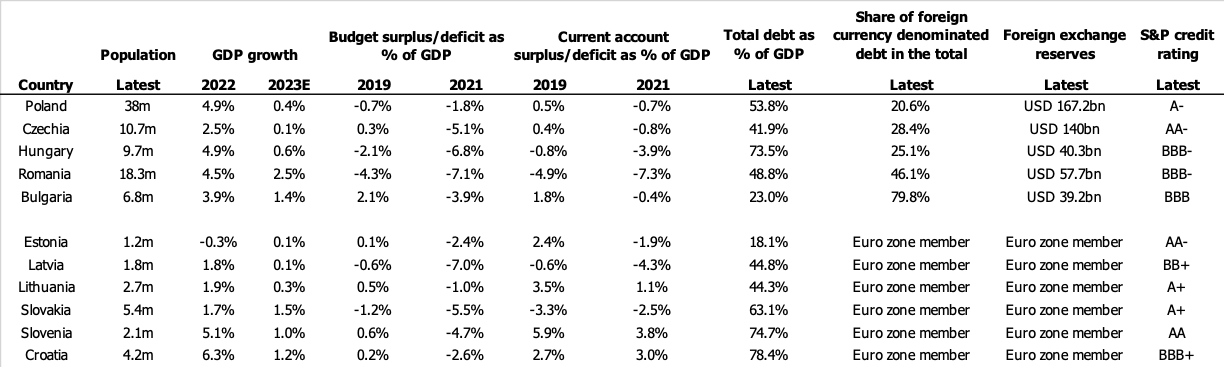

Trump’s plans could have severe economic and political consequences for the EU. His tariffs would likely hit Germany — the largest European economy and home to a car & machine building industry that support c. 800,000 and c. 955,000 jobs respectively — particularly hard. For most EU countries, including those in Central and Eastern Europe, Germany is by far the largest trading partner. For example, it currently accounts for approximately 27% of Poland’s exports, 33% of Czechia’s, 26% of Hungary’s, and 21% of Romania’s. Unless Europe quickly reduces its dependence on the US and China, the likely outcome could be a deep, Europe-wide recession, deindustrialization, and significant long-term destruction of wealth.

In terms of defense policy, a forced peace deal in Ukraine — under which Russia would likely retain the territories it has already seized, likely resulting in even more Ukrainian refugees in Western Europe — would have mixed implications. While Europe might participate in the rebuilding of Ukraine, the negatives would likely outweigh the positives. Reports suggest that members of Trump’s inner circle want Europe to bear the cost of securing a planned demilitarised zone between Ukraine and Russia’s occupied territories such as Donbas. Additionally, the EU would need to significantly increase its defense spending to deter further aggression from Russia.

In our view, sectors in Europe that could benefit from this new reality include defense, construction (particularly companies with prior experience in the CIS region), building materials, mining (e.g. producers of coke coal that is critical for steel production), and steel. Moreover, if a peace treaty is signed, the following Ukrainian companies — most of which are listed in Warsaw — could see significant recovery: Astarta, Ferrexpo, IMC, and Ovostar Union. However, we must emphasise that investing in Ukrainian equities carries significant risks, as these companies often lack adherence to Western corporate governance standards, and minority shareholder rights are frequently disregarded.

{kind=link}