2023 has been a very successful year for XTPL. The company signed various new distribution agreements (e.g. with Detekt Technology for Taiwan, with CWI Technical Sales & Ontos Equipment System INC for North America) and received new patents (e.g. in Malaysia, US, Germany, China, Vietnam). While the number of Delta Printing Systems sold was higher than we had expected (13 vs. 12), 5 thereof will only be included in the company’s results in 2024E. The number of sold printing heads was lower than we had forecast (3 vs. 5).

In 9M/23, XTPL’s revenues from sales of products and services reached PLN 9.2m, which corresponds to a y-o-y growth of 38.2%. Thereof, PLN 417k (+155.2% y-o-y) stemmed from sales of nano inks, PLN 2.7m (-41.1%) from R&D services and PLN 6.1m (+220.4% y-o-y) from sales of Delta Printing Systems. In 9M/23, EBITDA equalled PLN -1.2m (9M/22: PLN -1.3m) and net income PLN -2.6m (PLN -2.1m). Operating cash flow (PLN -3.1m vs. PLN 1.1m) was weaker than last year following a PLN 1.7m increase of working capital. Due to the capital increase in July, which had a volume of PLN 36.6m gross (275,000 shares at PLN 133), the company’s cash position reached PLN 31.7m. At the end of September, XTPL had interest-bearing debt of PLN 4.2m, of which PLN 3.9m was short-term (thereof, PLN 3.2m of bonds that will be converted into 45,655 shares at, we believe, PLN 74 per share, according to a public announcement from January 15th, 2024).

As of 30/09/2023, XTPL had 61 employees compared to 45 as of 31/12/2022. Thus, within 9 months the number of staff increased by >35%.

Our new forecastsfor 2024E and beyond

As in 9M/23 XTPL’s results were below our expectations and in H2/23 the company started the planned investments in sales and production capacity – according to its strategy, it wants to invest c. PLN 60m by 2026E among others in own sales offices/show rooms in Taiwan, South Korea and the US – we now believe that revenues in 2023 reached PLN 12.2m (prev. PLN 17.8m) and EBITDA PLN -2m (PLN -665k).

In our view, 2024E will be a breakthrough year for XTPL as we expect the start of the first full-scale commercial integration of its technology in H2/24E (currently, it has 9 industrial projects in the pipeline). This will allow the company to significantly increase recurring sales of its high-margin nano inks.

Conclusion

In conclusion, our optimism for XTPL remains steadfast. The company’s strategic approach is proving effective, evident from the consistent announcement of new sales contracts and distribution agreements at regular intervals. Anticipating a break-even on all levels by the end of the fiscal year 2024E, we do not foresee the need for another capital increase in the near future.

Notably, XTPL’s cutting-edge technology has undergone testing and validation by partners in Asia, including Nano Dimension from Israel and HB Technology from South Korea. Moreover, signs point to its adoption by prominent tech companies in the United States. A recent job posting by META seeking a Research Scientist Intern with experience in handling XTPL printing technology strongly suggests the integration of XTPL’s technology within this FAANG company (link: https://www.metacareers.com/jobs/880047783530931/).

On October 15, 2023, the parliamentary election were held in Poland. The incumbent socially conservative political party, Law and Justice (PiS) faced strong opposition primarily from the Civic Coalition (KO), representing the centre to centre-left. The voter turnout reached 74.4%, marking the highest in the history of Third Polish Republic since 1989. Although PiS had governed independently since 2015, the election results indicated that to continue, they would need to form a coalition with another political alliance.

Other parties that surpassed the 5% threshold in the elections included the Third Way (centre to centre-right), New Left (left), and Confederation (right to far-right).

Eight years of PiS rule can be summarized as a period of strengthening and favouring state-owned companies, significantly impacting the banking and energy sectors. The ruling party justified these initiatives as necessary measures to exert control over strategically important sectors of the Polish economy. For example, the Polish government acquired – indirectly through the largest Eastern European insurance group PZU – a controlling stake in the second largest Polish bank Pekao S.A. (PEO) from Italian Unicredit and merged its oil company Orlen (PKN) with another oil refiner & producer Lotos, the gas explorer & producer PGNiG and the utility Energa.

The introduction of the bank asset tax in 2016, excluding government bonds, resulted in an increased reliance on banks for financing public debt and negatively affected the profitability of the banking sector. As of the end of March 2023, government and guaranteed bonds in the banks’ portfolios amounted to approximately PLN 450bn, constituting about 20% of the banking sector’s assets.

As a result of the election, the five aforementioned political alliances secured seats in the Sejm. PiS obtained 194 seats, KO – 157, the Third Way – 65, the New Left – 26, and the Confederation – 18. To achieve a majority, 231 seats are needed. President Andrzej Duda (PiS) entrusted the winning party PiS with the formation of the government, but the opposition that has been formed after the election (KO, New Left, Third Way) has already reached an agreement to create a coalition. If successful, this coalition, led by Donald Tusk, the former President of the European Council, would have the majority in both the Senate and the Sejm. This newly formed coalition would also enable the rebuilding of relations with European Union (EU) and access to frozen funds from the national recovery and resilience plan (RRP) for Poland.

National Recovery Plan

Poland was initially expected to receive the first tranche of funds in June 2022, but this did not happen. A crucial factor in accessing funds from the RRP is meeting the requirements of the so-called “milestone” conditions. The primary cause of the delay in disbursement of funds by the EU was a dispute with the Polish government over the independence of the judiciary. On November 21, 2023, the recently revised plan, with a base budget amounting to EUR 59.8bn (PLN 270bn) was accepted by the European Commission. Out of this substantial sum, EUR 25.3bn will be provided in the form of grants and EUR 34.5bn as loans.

We anticipate that, following the establishment of the government of Donald Tusk, Poland will promptly fulfil milestone conditions and receive funds according to the new schedule. The plan consists of 7 key components, and we find two components of this plan noteworthy for their potential impact on companies listed on the Warsaw Stock Exchange and the overall economy.

Component G: According to the plan for the allocation of funds, over EUR 25bn is earmarked for the REPowerEU program, aiming to reduce reliance on fossil fuels before 2030 and transition into renewable energy sources. Poland will soon receive a pre-financing instalment of EUR 5bn for the implementation of the REPowerEU changes. According to the European Commission, EUR 21bn in costs related to REPowerEU will require multinational cooperation. Worth noting is the allocation of EUR 17bn to the Energy Support Fund, which will finance investments related to the energy transition, and the allocation of EUR 4.8bn to the construction of offshore wind farms.

Component B: Over PLN 20bn is allocated to green energy and reduction of energy-intensity, supporting the increase in the use of alternative energy sources and improving the energy efficiency of the Polish economy. This component is related to REPowerEU as it addresses decarbonisation and air pollution in Poland. Similarly, it presents an opportunity for renewable energy companies as well as for firms cooperating with them. Additionally, there is a target reduction of energy consumption by renovating buildings, providing an investment opportunity for construction companies, for example Izolacja Jarocin (IZO), Selena FM and Ferro.

In summary, the RRP funding should help the EU to achieve its ambitious goal of becoming climate-neutral by 2050, with 46.6% (EUR 27.8bn of 59.8bn) allocated to climate contributions. The remaining components of the plan include: resilience and competitiveness of the economy, digital transformation, effectiveness | availability and quality of the health care system, green and smart mobility, Improving the quality of institutions and the conditions for the implementation of the RRP. link to the European Commission’s publication on the proposal

What is next after elections?

Currently, PiS is attempting to secure the required majority of 231 mandates. Specifically, PiS is trying to persuade the Third Way to join them in a coalition, which seems unlikely to happen as the Third Way, in its electoral plan, includes postulates directly targeting PiS. Although over a month has passed since the election, and the most likely scenario is that the opposition coalition (KO, New Left, Third Way) will form the government, there is still a lot of uncertainty.

In the electoral plans of the parties, forming the opposition coalition, there is a lack of specific demands regarding the stock exchange, and economic issues are somewhat overshadowed by primarily social matters. The main topics related to publicly traded companies include the depoliticization of state-owned companies, obtaining funds from the aforementioned recovery and resilience plan, investing in renewable energy sources, and the abolishment of the capital gains tax for savings and investments.

We believe that the abolition of this tax could lead to an increase in the share of individual investors, consequently boosting liquidity on the polish stock exchange, which is far lower than in western markets. Nevertheless, there is a relatively high chance that this tax abolition will be just an unfulfilled election promise, as within the coalition there is a leftist party that will likely oppose it and such a tax is common in other European countries.

In our view, there is a chance that state-owned companies, many of which are trading far below their book values and at low single-digit P/Es, will perform well over the next months as investors hope that the new KO-led government will improve corporate governance, rights of minority shareholders and dividend payouts. The last few weeks have shown that international investors have already become more active especially in the bluechip WIG20 index (it has increased by c. 28% over the last 3 months). We believe that if the new government really was to fulfil its promises, the whole Polish capital market would significantly benefit.

This blog post marks the beginning of a series of analyses focused on Polish companies and their listed direct German counterparts.

In this installment, we will delve into the examination of Oponeo.pl S.A., a company listed on the main market of the Warsaw Stock Exchange since 2007, and Delticom AG, headquartered in Hannover. Delticom AG holds the position of a European leader and has been listed on the Frankfurt Stock Exchange since 2006.

History & current business

Oponeo.pl was founded in 1999 by university friends Dariusz Topolewski and Ryszard Zawieruszynski, who continue to own and manage the company today. It is headquartered in Bydgoszcz, Poland. Over the years, the company has grown to become the largest online retailer of tires and rims in Poland, holding a market share of over 75%. In recent years, Oponeo has expanded its operations to 12 foreign markets, primarily in EU countries but also in Turkey. The company has successfully established or acquired other e-commerce businesses, including Dadelo, an online shop for bikes and sports accessories that is also listed on the Warsaw Stock Exchange, and Rotopino.pl, an online retailer of tools. Oponeo Group currently operates 25 online shops, employs 348 individuals, and owns a modern, automated warehouse in Poland spanning 72,000 square meters. Additionally, Oponeo has formed partnerships with over 1,000 fitting service providers in Poland and more than 3,000 in its other markets. The company relies on wholesalers and producers for distribution to foreign clients.

Delticom, also founded in 1999, has become the largest online retailer of tires and rims not only in Germany but also across Europe. While Delticom faces strong competition from Oponeo in countries like the Netherlands and Belgium, it held a presence in the United States until 2022, when Delticom North America was sold (the transaction generated a one-off gain of EUR 3.8m). In 2016, Delticom’s founders, Andreas Prüfer, Rainer Binder, Philip von Grolman, and Timon Samusch, attempted to diversify their business by acquiring an online distributor of used cars in France and online shops for gourmet and regular food in Germany. However, due to liquidity issues, these diversification efforts were ultimately discontinued in 2019-2020. Presently, Delticom has refocused its efforts on its core activity of selling tires and rims. The company operates approximately 300 online shops in nearly 50 countries, employing 168 individuals. Delticom runs warehouses in Sehnde, Germany (over 60,000 square meters), and Ensisheim, France (around 50,000 square meters).

Historical & current financials

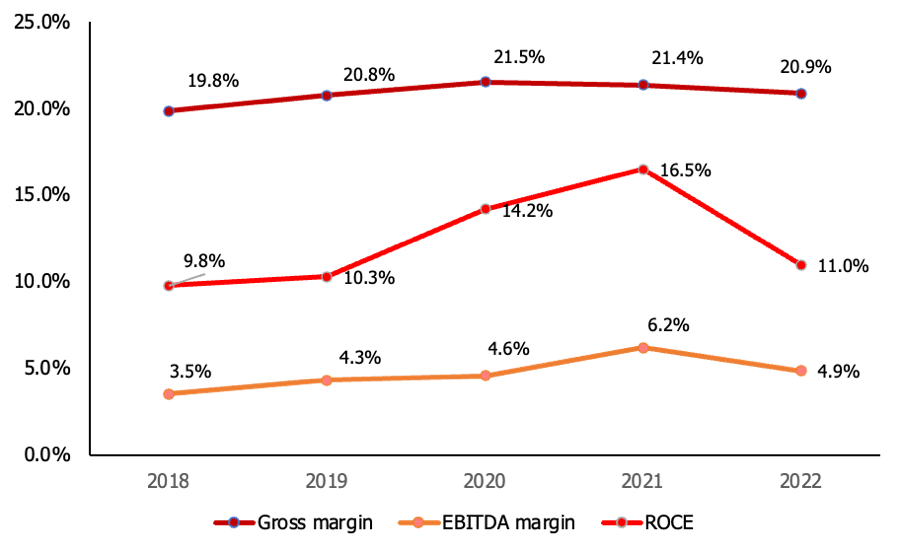

Oponeo boasts an impressive track record when it comes to its financial performance. Between 2012 and 2022, the company managed to increase its revenues from PLN 207.1m to PLN 1.7bn, achieving a CAGR of 23.4%. Concurrently, its EBITDA also saw a substantial rise, climbing from PLN 6.7m to PLN 82.5m (CAGR of 28.5%). Over the past five years, Oponeo has maintained EBITDA and ROCE figures within the range of 3.5% to 6.2% and 9.8% to 16.5%, respectively.

Since 2008, Oponeo has consistently been distributing dividends to its shareholders and has also regularly engaged in stock buyback initiatives. Despite the challenging situation prevailing in the retail sector at present, the company displayed notable resilience. In the first half of 2023 (H1/23), Oponeo achieved a year-on-year revenue growth of 14.1%, amounting to PLN 789.4m. However, there was a decline of 9.6% in EBITDA, reaching PLN 18.9m during the same period. The company has managed to maintain a reasonably low net gearing level of 11.3%.

Oponeo.pl S.A.: Gross & EBITDA margins and ROCE in 2018-2022

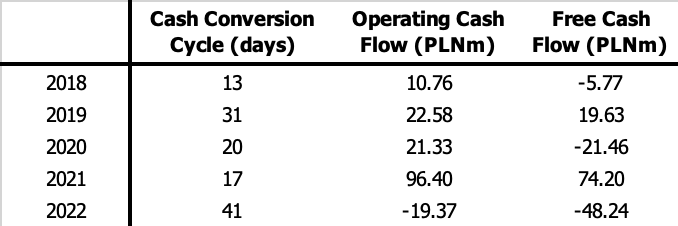

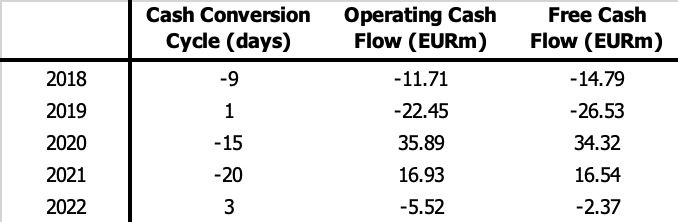

Oponeo.pl S.A.: Cash Conversion Cycle, Operating and Free Cash Flow in 2018-2022

Source: Company information, East Value Research GmbH

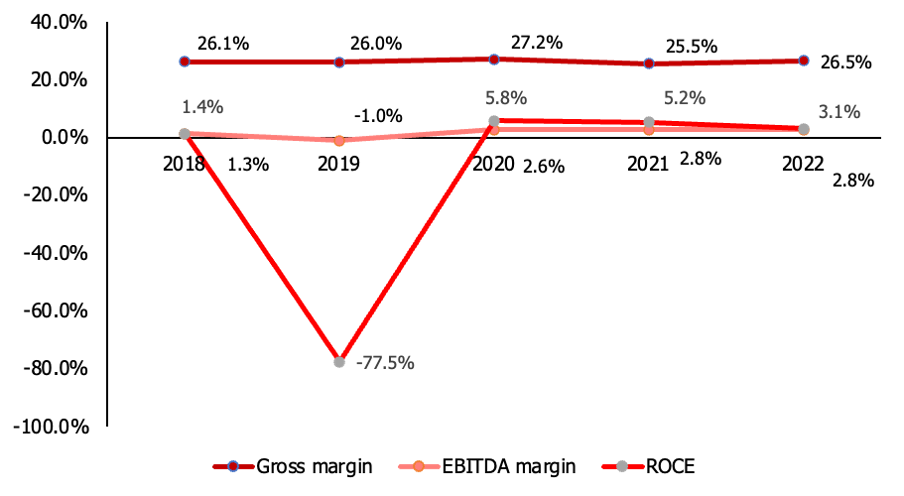

An examination of Delticom’s historical performance presents a mixed overview. Between 2012 and 2018, the company experienced a consistent growth in sales, averaging a 6.5% increase annually, accompanied by a clearly positive EBITDA margin. However, due to an unsuccessful expansion into the online food business, the company’s profitability suffered a steep decline in 2019. During that year, Delticom reported an EBITDA of EUR -6.6m and an EBIT of EUR -42.1m. Consequently, the company’s net debt escalated to EUR 87.8m, causing a substantial drop in Delticom’s share price from its peak of around EUR 80 in 2011 to below EUR 3.

Nonetheless, following a restructuring effort, the company managed to restore a positive operating profit trajectory. Presently, Delticom is poised to achieve an estimated EBITDA of approximately EUR 14m this year. In the first half of 2023, the company’s revenues experienced a year-on-year decline of 10%, amounting to EUR 197.7m. This contraction was primarily attributed to a redirection of revenues towards Delticom’s newly established marketplace, Reifen.com. Within this platform, the company sells car accessories from third-party retailers, earning commissions.

The net gearing ratio stood at 200.5%, but this included an estimated EUR 50m of IFRS 16 related leasing debt, thus the actual net debt figure was not EUR 82.8m but EUR 32.8m (equity equalled EUR 41.3m). At the end of 2021 and 2022, the respective net gearing amounted to 138.5% and 178% respectively. In H1/23, the increase was driven by the accumulation of inventories in preparation for the crucial winter season, a common practice in Delticom’s sector. However, it is anticipated that by the end of 2023, the net gearing ratio will once again substantially decrease compared to the value recorded as of June 30, 2023.

Delticom AG: Gross & EBITDA margins and ROCE in 2018-2022

Source: Company information, East Value Research GmbH

Delticom AG: Cash Conversion Cycle, Operating and Free Cash Flow in 2018-2022

Source: Company information, East Value Research GmbH

Current valuation & conclusion

Compared to Delticom, Oponeo has a more favorable track record, and we possess greater confidence in its management. Nevertheless, we believe that much of this positivity is already factored into the company’s current valuation metrics. For instance, Oponeo’s estimated enterprise value to sales ratio (EV/Sales) for 2023E is 0.3x, which is in line with the 5-year average of 0.4x. Similarly, its EV/EBITDA ratio for 2023E is 7.7x compared to the 5-year average of 6.7x.

On the other hand, Delticom presents an intriguing restructuring narrative, particularly due to its current historically low valuation. The projected EV/Sales ratio for 2023E is 0.2x, consistent with the 5-year average. Likewise, the projected EV/EBITDA ratio for 2023E is 6.9x as opposed to the 5-year average of 9.9x. Notably, Delticom exhibits a notably higher revenue per employee compared to Oponeo, amounting to EUR 1.18m versus EUR 507.5k.

Assuming that inflationary pressures ease, which we anticipate occurring in Q4/23E, and if online sales rebound, Delticom’s financial performance and market valuation are likely to follow suit. A scenario reminiscent of 2020-21 could emerge, wherein Delticom experienced a significant improvement in EBITDA compared to 2019, leading to a substantial increase in its stock price. During the period between mid-2020 and mid-2021, the stock price surged from a low of approximately EUR 2.50 to EUR 9.70. Although we believe the potential return currently exceeds 100%, it’s important to acknowledge key risks such as elevated net gearing and concerns surrounding Delticom’s founder and CEO, a figure who generates controversy among institutional investors. Nevertheless, we hold the view that the company’s prevailing trading multiples already adequately account for these factors.

In Q1/23, XTPL generated revenues of PLN 3 million from sales of products and services, representing a significant year-on-year growth of 219.9%. Revenues from grants amounted to PLN 605k (compared to PLN 689k in Q1/22). The gross margin stood at 60.4% (compared to -29.4% in Q1/22). After accounting for operating expenses of PLN 2.2 million, XTPL achieved an EBITDA of PLN 78k (compared to a loss of PLN -2.4 million). Net income improved from a loss of PLN -2.7 million in Q1/22 to a loss of PLN -301k.

During this year, XTPL announced five contracts for the sale of Delta Printing Systems, all of which were sold to Chinese clients. Additionally, two contracts were signed for printing modules, with buyers including HB Technologies, a supplier of machines for testing and repair of displays for companies like Samsung Display and Beijing BOE Display. Furthermore, a large US-based NASDAQ-listed producer of machines for the semiconductor industry (likely Lam Research Corp., with a market cap of USD 82.3bn and yearly sales exceeding USD 17bn) also purchased printing modules. According to sources such as Pocket-lint and 4kfilme, Samsung Display delivers 80 million OLED displays solely for the iPhone 14 and produces over 100,000 Quantum Dot (QD)-OLED displays for TVs each month. In our view, considering that more than 10% of these displays typically have defects, this demonstrates the significant commercial potential for XTPL.

Issuance of new equity and debt for capacity expansion and building of local sales teams

XTPL announced its intention to issue up to 275,000 new shares on May 12th, which will finance approximately 50% of the planned investments amounting to PLN 60 million from 2023E-26E. The remaining funding will come from own funds, grants, and new debt. The equity issue, in which the CEO and founder also intends to participate, is expected to be completed this week. Our research indicates that debt financing has already been secured.

According to discussions with management, the PLN 60 million will be allocated towards several initiatives, including:

Expanding the production capacity of printing modules from the current level of less than 10 per year to 100 per annum (which would correspond to yearly sales of EUR 7.5 million/PLN 33.75 million).

Increasing the production capacity of prototyping machines, specifically the Delta Printing System, from currently more than 10 units to more than 20 units per year (e.g., 20 units would equal yearly sales of EUR 3.5 million/PLN 15.75 million).

Quadrupling the yearly production of nanoinks.

Establishing local sales offices with demonstration labs primarily in the US and Asia, a strategic move to accelerate the acquisition of new clients.

Hiring additional staff and continuing research and development activities.

Expected boost for XTPL’s business from Intel’s new factory near Wroclaw

Moreover, XTPL is expected to benefit from Intel’s new factory near Wroclaw, announced on June 16th. The US semiconductor giant’s investment of USD 4.6 billion/PLN 18.4 billion in a new factory for semiconductor integration and repair in Miekina, approximately 30 km from Wroclaw, is the largest foreign investment in Poland to date. Given that semiconductor and display repairs align with XTPL’s technology applications, Intel could become a potential client for XTPL.

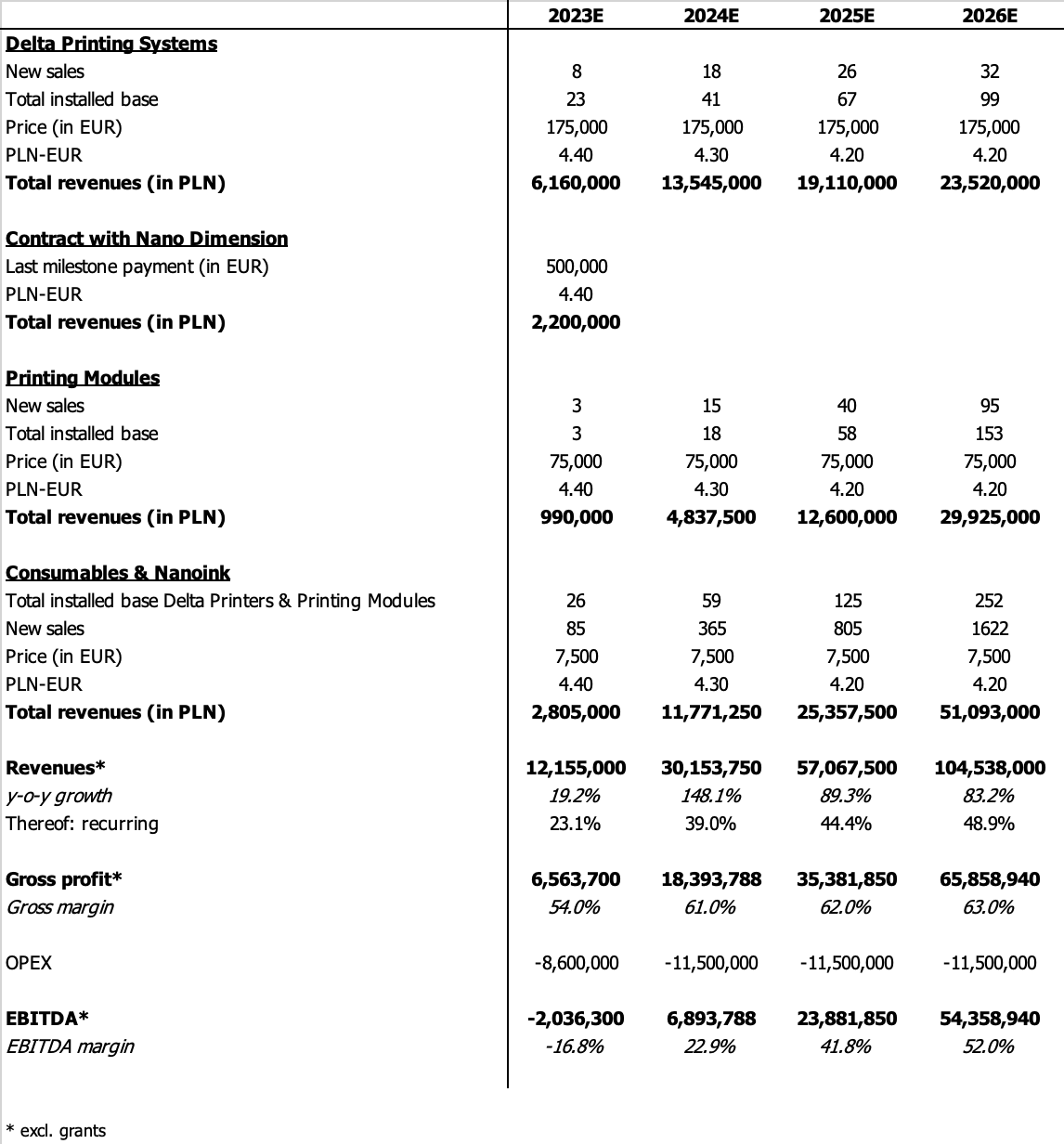

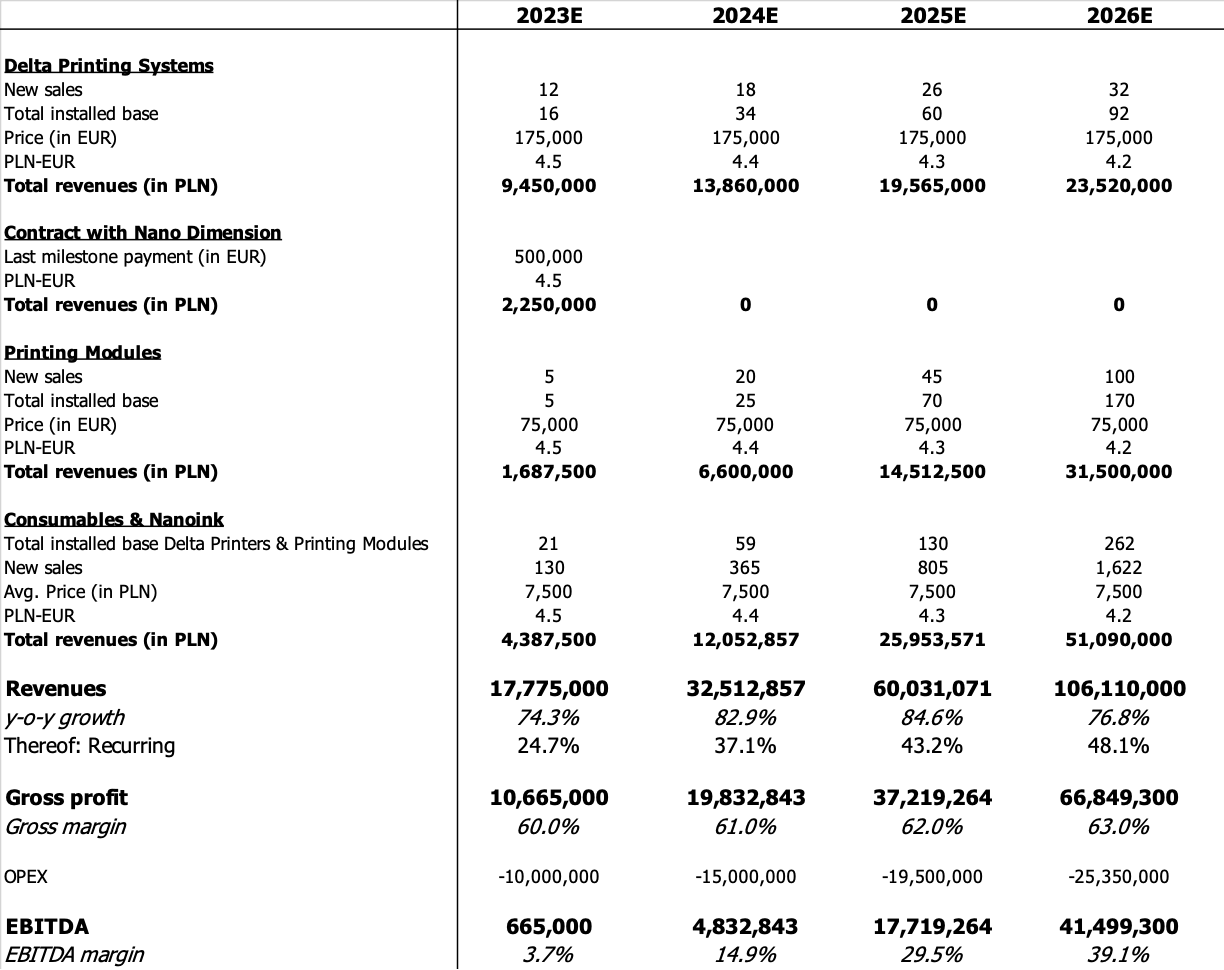

Our forecasts for 2023E-26E imply a revenue CAGR 2022-26E of 60.2% and a target EBITDA margin of c. 40%

We have constructed a financial model for XTPL that extends until 2026E and takes into account the latest information provided by the company’s management. Our projections are slightly more optimistic than the company’s own guidance, which anticipates sales of PLN 100 million in 2026E.

What sets XTPL’s business model apart is the increasing number of Delta Printing Systems and Printing Modules being sold, which will drive recurring revenues from consumables and inks. This will ultimately result in substantial double-digit EBITDA margins.

While we initially anticipated a net profit for the current fiscal year (2023E), we now believe that planned investments, such as the establishment of local sales teams in the US and Asia, will likely lead to a negative net income. However, we are highly optimistic that 2024E will mark XTPL’s first profitable year.

Conclusion

In conclusion, XTPL’s technology commercialization appears to be on track, as promised by CEO and founder Filip Granek. The demand for the company’s products is evident from major international research facilities and industry players. Furthermore, with a significant share of high-margin recurring revenues expected to exceed 48% by 2026E, XTPL’s commercialization model holds significant appeal.

We have confidence in our estimates, projecting a sales CAGR of 60.2% from 2022 to 2026E, along with target EBITDA margins of approximately 40%. For only one of their projects, industrial clients such as HB Technologies or Lam Research could potentially purchase up to 100 printing modules, which will need to be replaced after 5 years. As production volumes increase, these modules will generate a rapidly growing stream of recurring revenues from consumables and nanoinks, resulting in a significant operating cash flow for XTPL.

With currently 777 listed companies (main regulated market + the alternative NewConnect segment), a combined market capitalization of PLN 1.3tr/EUR 285.9bn and a daily turnover of PLN 1.1bn/EUR 249.1m, the Warsaw Stock Exchange is by far the largest and most liquid stock exchange in Emerging Europe.

Given the economic catchup potential of the region, other capital markets are also worth a look, however they are usually characterized by very low trading volumes. In general, the value of listed stocks in Central and Eastern Europe (CEE) & South-Eastern Europe (SEE) is much smaller in terms of the market capitalization-to-GDP ratio than of Western markets.

Sources: World Bank, CEIC, GuruFocus, East Value Research GmbH

Czech Republic

In Prague, the combined market capitalization of local stocks equals c. EUR 55.7bn and the daily turnover amounts to c. EUR 93m. The largest companies are the utility CEZ, the tobacco producer Philip Morris CR and the banks Moneta Money Bank and Komercni Banka. All these stocks can also be traded via dual listing in Frankfurt. There is also the alternative START segment for small- and medium-sized Czech companies.

Hungary

In Hungary, the stock exchange has 69 companies, a combined market cap of c. EUR 35bn and a daily turnover of c. EUR 22.6m. The largest companies are from traditional sectors: OTP (the largest Hungarian bank), MOL (Oil & Gas), Gedeon Richter (one of the largest generic producers in CEE), Magyar Telecom (the largest Hungarian Telco). All of them also have a dual listing in Frankfurt. In 2017, the Hungarian stock exchanged launched a dedicated segment for small- and medium-sized companies, which is called Xtend.

Romania

With 19.1m inhabitants, Romania is the second most populous country in CEE & SEE after Poland. At 359 (84 in the main market and 275 in the alternative AeRO segment), its stock exchange has the second-highest number of listed companies in the region. Their combined market capitalization equals EUR 44.7bn. While liquidity is a major issue, investors can find very promising stocks, some of which with consistently high dividend yields. The largest of them are: OMV Petrom (an oil & gas company that is owned by Austrian OMV Group), SNGN Romgaz (a state-controlled gas company), SNN Nuclearelectrica (a state-controlled utility), Banca Transilvania (No 1 bank in Romania), and Fondul Proprietatea (an investment holding that invests in listed and privately held Romanian companies and is managed by Franklin Templeton. These companies can also be traded on foreign exchanges e.g. in London.

The Baltic countries

In the Baltic region, the companies are listed on the NASDAQ Baltic exchange, where there are currently 55 companies, thereof 24 from Lithuania, 11 from Latvia and 20 from Estonia. Their combined market capitalization equals EUR 10.4bn and daily turnover EUR 2.3m. The largest companies on the NASDAQ Baltics are Ignitis Group (a Lithuanian utility), Telia Lietuva (Telco), Enefit Green (an operator of renewable energy production units in the Baltics and Poland) and LHV Group (an Estonian bank).

The Balkan region

In the Balkan region, each country has its own stock exchange, but most are very illiquid. For example, in Belgrade the daily turnover of all listed stocks only equals c. EUR 44k. The largest stock exchange in the region is the one in Zagreb (market cap of all traded domestic stocks: EUR 19.6bn), followed by Ljubljana (combined market cap of EUR 8.9bn). In Zagreb and Ljubljana, the average daily turnover equals c. EUR 908k and EUR 1.1m respectively and the largest companies in terms of market capitalization are the oil & gas company INA, the leading bank in Croatia Zagrebacka Banka, the producer of generic drugs Krka and the Croatian Telco Hrvatski Telecom.

According to latest data published last week, the assets of PPKs already reached PLN 14.9bn/EUR 3.2bn. The pension plans, which were only introduced in 2019 and are co-financed by employees, employers and the Polish government, are quickly adding participants, with 3.3m (43.7% participation rate) of employees already in the program. Only in the last two months, the number of new participants has grown by 718k due to an automatic subscription, which is conducted every 4 years of 18-55 year old employees, who previously decided to not participate in the PPKs.

Currently, PPKs, which are managed by private investment management firms, are adding PLN 500m/EUR 98m of assets per month, of which up to 70% – dependent on the age of the employee – can be invested in stocks (in case of <40 years olds, the share can equal max. 70% and for the age group 60+ max. 15%). Thereof, at least 40% of assets must be invested in Polish blue chips (WIG20 index). PPKs are also allowed to invest max. 20% of their assets dedicated to equities in Polish midcaps, max. 10% in smallcaps (incl. from the alternative Newconnect segment) and min. 20% on foreign stocks exchanges.

Latest forecasts foresee an increase of the share of PPK participants to 50% within the next 2 years. Monthly new assets should grow accordingly. This should positively impact the daily trading turnover on the Warsaw Stock Exchange and thus make the Polish capital market more attractive for foreign institutional investors.

In December 2022, the Polish capital market had a record low CAPE (= inflation-adjusted 10y average P/E ratio) of only 7.1x vs. 16.7x for Deutsche Börse and 28.4x for the NYSE. While Poland’s economy has been growing rapidly in the last years with yearly GDP growth rates of 3-6%, the stock market – and the bluechip WIG20 index in particular – have not kept pace. The WSE is the largest stock exchange in the CEE region with 754 listed companies. The No 2 – the stock exchange in Sofia – has 255 companies.

Given the above, the German economy faces two main risks: 1. High energy prices in the long run, especially as Germany is the only country worldwide, which plans to completely withdraw from fossil energy and nuclear power so fast, and 2. A China-Taiwan war. The first scenario would likely result in the movement of production capacity – and loss of high-paying jobs – from Germany to other parts of the world. Especially, North America seems to be an attractive destination as it has access to cheap energy and is a net exporter of it. The second would significantly negatively affect the German economy as a conflict in Taiwan would likely result in sanctions by the US and the EU like those imposed on Russia after its invasion in Ukraine in February 2022.

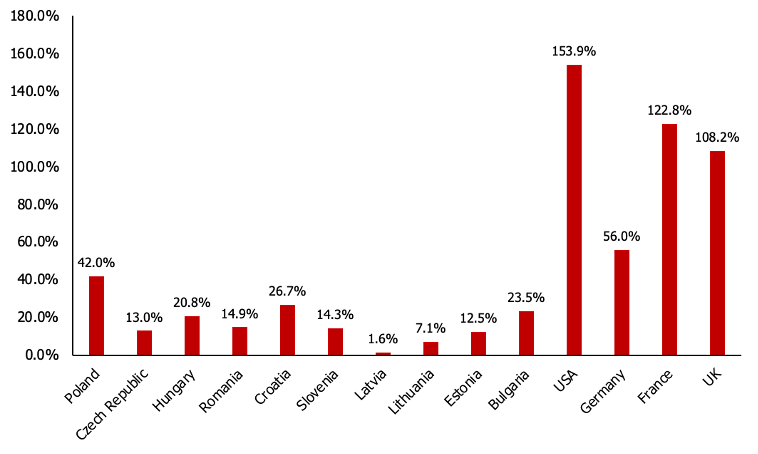

While we believe that especially the 2nd scenario seems unlikely for now as China needs the Western world as a trading partner – USA and Germany were its No 1 and 7 trade partners respectively in 2022 and the EU as a whole No 2 after ASEAN – and supplier of advanced technology, the above-mentioned factors also bear significant risks for Eastern European countries. For most of them, Germany is the largest trading partner by far (see table below) and a significant share of employees has jobs in German companies or their suppliers. For example, automobile producers such as VW Group (9 in Poland, 4 in the Czech Republic, 2 in Slovakia, 1 in Bosnia, 1 in Hungary), Mercedes-Benz (1 in Poland, 1 in Romania, 1 in Hungary) and BMW (1 in Hungary) have many production facilities in the CEE/SEE region. The same holds for chemical companies – which are particularly energy-intensive – such as BASF (19 production facilities in CEE) and Lanxess (3).

CIECH, which is based in Warsaw, is an international chemical group with factories in Poland, Germany, Spain and Romania, >3,000 employees and a worldwide customer base. It is the 2nd largest manufacturer of sodium carbonate and sodium bicarbonate in the EU, the no 1 manufacturer of evaporated salt in Poland, the no 1 supplier of sodium silicates in Europe, the largest Polish manufacturer of plant protection products, and a leading Polish producer of polyurethane foams in Poland. CIECH’s products are crucial elements in different industries incl. Construction, Automotive, Agriculture, Chemical, Food and Pharma. They are used in the production of articles necessary in everyday life.

In 2021, Poland was CIECH’s largest geographical market with a share of 51%, followed by other EU countries (45%), other Europe (2%) and Asia/Africa/Other (2%). The Soda segment was the company’s largest one by far and accounted for 66% of total sales and c. 81% of adjusted EBITDA. Its products soda ash, sodium bicarbonates and salt are used in the production of flat glass, glass packaging, silicates, detergents, animal feed, food, and water treatment solutions, among others. Other segments include:

Agro (crop protection products, herbicides) – 14% of total sales in 2021 and c. 16% of adj. EBITDA

Foams (Polyurethane foams that are mainly used in the production of furniture and matrasses) – 11% of revenues and >16% of adj. EBITDA

Silicates (sodium and potassium silicates used e.g. in the production of precipitated silica, paper and welding electrodes) – 7% of 2021 sales and >4% of adj. EBITDA and

Packaging (lanterns for vigil lights, jars) – 2% of total sales and >2% of adj. EBITDA

CIECH S.A. has been listed on the Warsaw Stock Exchange since 2005. It can also be traded in Frankfurt. Since 2014, the company has been owned by Kulczyk Investments, which belongs to the 6th richest Pole Mr Sebastian Kulczyk. Kulczyk Investments (through KI Chemistry) bought a control stake of 51.1% in CIECH from its previous owner, the Polish state, at PLN 31 per share.

Financials

In 2021 – the last fiscal-year, for which results are available – the CIECH Group generated revenues of PLN 3.5bn (+16.3% y-o-y, 5y CAGR of 0.03%), an EBITDA of PLN 730.4m (+24.1%, 21.1% margin, 5y CAGR of -3.9%) and a net income of PLN 292.4m (+126.2%, 8.5% margin). Operating and free cash flow equalled PLN 1.3bn (2020: PLN 767.2m) and PLN 571.5m (PLN -66.8m) respectively. Between January and December 2021, CIECH’s ROCE equalled 5.8%, while we estimate its current WACC at 14.2%, implying that the company is not generating a sufficient return on the capital employed to offset its costs of capital.

In 9M/22, the company generated revenues of PLN 3.9bn (+57.4% y-o-y), an adj. EBITDA of PLN 661.2m (+19.3%) and net income of PLN 234.5m (+0.2%). At the end of September, its net gearing equalled 56.1%.

In the last years, CIECH has paid out dividends, but not regularly. For 2022, the company paid out PLN 1.50 per share, which corresponds to a DYield of 2.9% at present.

Comment on the tender offer

On March 9, Kulczyk Investments through its subsidiary KI Chemistry Sarl announced a tender offer for all the remaining 48.86% shares of CIECH Group at PLN 49 per share, which starts on March 10 and is supposed to end on April 12. After reaching a threshold of at least 95% of the shares outstanding, Kulczyk Investments plans to delist CIECH as it believes that as a listed company it cannot “react in a fast and flexible manner to rapidly changing economic, geopolitical and regulatory environments, and turbulences on global financial and raw material markets”.

In our view, the tender price is far too low and does not reflect CIECH’s fair value. The current share price of PLN 52.35, which is 6.8% above the tender price, implies an EV/EBITDA 2023E and P/E 2023E of 3.9x and 6.8x respectively. The 5-year hist. average EV/EBITDA and P/E multiples of 5.1x and 11.5x respectively are 31.3% and 69.8% higher.

We expect that especially the Polish investment and pension funds, which hold approx. 27% of CIECH’s shares at present, will urge Kulczyk Investments to increase the tender price. Consequently, we advise current investors not to sell their shares in the tender and to increase their stake in the company.

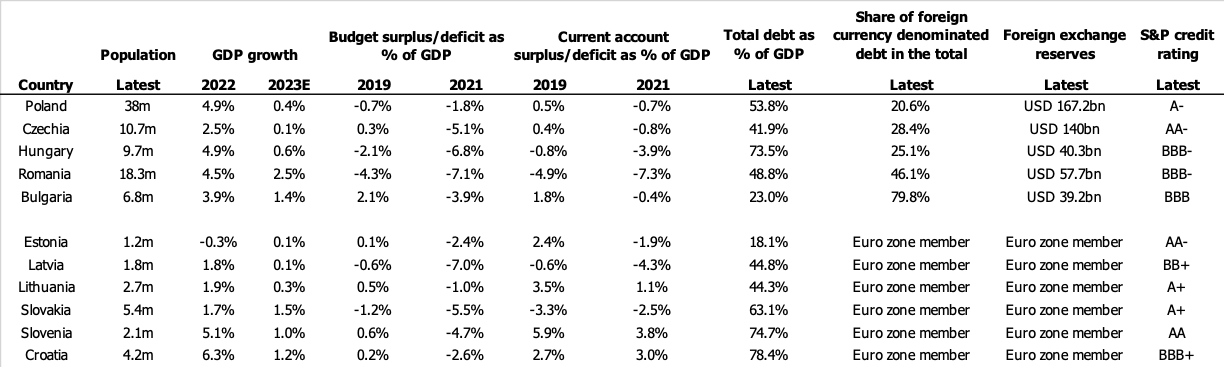

In this blog post, we analyze the public finances of the EU member states that before 1990 were part of the Soviet bloc. Slovenia, Slovakia, Croatia, Estonia, Latvia, and Lithuania are already members of the Euro zone and thus do not have control over their currency. When it comes to the budget and current account deficits, we have compared the most recent data from 2021, which was affected by the pandemic, with the pre-COVID year 2019. While our analysis concludes that Poland, Czechia, Estonia and Slovenia are relatively reliable debtors, the condition of public finances in Hungary, Romania and Bulgaria looks much riskier.

Sources: Eurostat, central banks, tradingeconomics.com, Worldbank, S&P, CIA World Factbook

Especially after the PiS (Law and Justice party)-led government came to power in 2015, the Polish economy has been supported a lot through various social programs e.g. the “500+” child benefit, “Dobry Start” PLN 300 one-off support for pupils and the one-off retirement payment of PLN 1,100 “Emerytura+”. While these programs are considered negative by many economists as they stimulate consumption instead of investments, apparently they have not increased the debt level as well as budget and current account deficits in Poland as much as similar measures in Hungary. Especially a high current account deficit, which reflects imports and exports of goods and services, payments to foreign holders of a country’s investments, payments received from investments abroad, and transfers such as foreign aid and remittances, can negatively affect the foreign exchange rate of a country’s currency. On the one hand, a weak currency makes exports more profitable, however on the other makes the import of important components, the servicing of foreign debt or popular consumption goods more expensive.

Apart from Poland, Czechia is another non-Euro country, whose public finances look solid. What is particularly impressive, are its significant foreign exchange reserves, which are 3.5 times higher than in Hungary that however has a similar population. The larger the foreign exchange reserves, the better a country can fight pressure on its own currency.

In Romania and Bulgaria, especially the relatively high share of foreign currency denominated debt is worrying, which can lead to issues with repayment of debt in case the local currency significantly weakens versus EUR or USD.

Based on the methodology of S&P, Hungary’s and Romania’s current BBB- rating is the weakest investment grade rating. The rating agency’s definition is as follows: “An obligation rated ‘BBB’ exhibits adequate protection parameters, however adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity of the obligor to meet its financial commitment on the obligation.” Estonia, whose debt only equals 18.1% of its GDP, and Czechia both have an AA- rating. According to S&P, it “differs from the highest-rated obligations only to a small degree”. Of all ex-communist EU member states, Slovenia has the best S&P credit rating (AA).

Founded in 1954 as a state-owned company, Krka, which is based in Novo Mesto/Slovenia, is among the world’s leading producers and developers of generic pharmaceuticals. In its own and leased production and R&D facilities in Slovenia, Croatia, Germany, Poland, the Russian Federation and China, the company employs c. 11,500 people. Generic medicines are original medicines, which have never had a patent protection or whose patent protection has expired. Both contain the same active pharmaceutical ingredients and are equivalent in terms of quality. So-called Super Generics are generics with an added value compared to their original drugs e.g. with improved pharmacokinetics, delivery or therapeutic effects. Their significant advantages are a shorter development (3-4 years vs. 12 years) and much lower costs (c. USD 50m vs. USD >1bn).

Krka distributes 800 pharmaceutical products and 600 formulations based on 250 APIs. It operates in the following business segments: Prescription & non-prescription pharmaceuticals targeting e.g. the areas cardiovascular diseases, central nervous system, gastrointestinal system, pain, infections, digestion, oncology and urinary tract (83.7% and 8.8% of total sales in 2021 respectively); Animal Health products (5.2%); and, through 100% subsidiary Terme Krka d.o.o, Health resort & tourist services (2.3%). Krka’s products, which are sold exclusively under the company’s own brands, are distributed in >70 countries worldwide. In 2021, 94% of total sales stemmed from outside Slovenia, thereof 35.1% from the East Europe region (former CIS region incl. Russia & Ukraine), 22.5% from Central Europe (mainly Poland, Czechia, Hungary and Lithuania), 19.5% from West Europe (e.g. Germany), 13.4% from South-East Europe (mainly Croatia, Romania and Bulgaria) and 3.4% from other markets in Africa, the Middle East and Asia.

Krka spends 9.9% of its yearly sales on R&D – is mainly related to oncology and autoimmune diseases, thus two of the largest segments of the global Pharma market – compared to 9.7% in case of its listed regional peer, Hungarian Gedeon Richter. It has c. 170 products in the pipeline in different R&D phases and has received/submitted patents for more than 210 innovations.

Krka, which has been listed since 1997, can be traded on the stock exchanges in Ljubljana, Warsaw and Frankfurt. The company has paid out a dividend in each of the last 11 years and since 2012 its DPS has increased at a CAGR of 13.8%. Only in 2017, the DPS was slightly lower y-o-y.

Krka’s largest shareholders are entities associated with the Slovenian state, which own in total 26.7% of the company’s shares and 35.7% of its votes. According to marketscreener.com, the company has both US-based and Western European investment funds as shareholders. The Norwegian sovereign wealth fund holds a stake of c. 0.8%. Treasury shares make up 5.5% of all shares outstanding.

Management’s 5-year guidance foresees a sales CAGR of at least 5% and an EBITDA margin of min. 25%.

Latest financials

In 2021, Krka, which before the pandemic grew at a 5y CAGR of 4.6%, produced c. 16bn (+2% y-o-y) pills and generated revenues of EUR 1.57bn (+2% y-o-y). With 18% and 9% respectively, the regions Slovenia and Other overseas countries reported the highest growth y-o-y. In 2021, the company introduced 16 new products. Drugs related to cardiovascular diseases accounted for >50% of all prescription drug sales.

Despite serious COVID-19-related shortages of materials and transport issues, between January and December 2021 Krka’s EBITDA reached EUR 463.6m (-7.7% y-o-y; 29.6% margin) and net income EUR 309.2m (+6.3%; 19.7% margin) respectively. While operating cash flow amounted to EUR 386.1m (2020: EUR 360.8m), free cash flow equalled EUR 13.5m (EUR 251.2m). In 2021, Krka generated a ROCE of 13.7% compared to 12.1% at Gedeon Richter.

For the first nine months of 2022, Krka reported revenues of EUR 1.24bn (+5.6% y-o-y). In Ukraine, where the company is the No 2 provider of generics, sales declined by -14% y-o-y, but in Russia, where it is No 4, they grew by 5%. In 9M/22, EBITDA reached EUR 314.2m (-10.9% y-o-y; 25.3% margin) and net income EUR 300.9m (+25%; 24.2% margin) respectively. The main factors, which affected profitability, were 9.6% higher CoGS y-o-y, 21% higher marketing & distribution expenses and a EUR 113.6m higher net financial result, which was positively affected by FX effects. At the end of September, the company’s net gearing amounted to -15.4% compared to 1% in case of Gedeon Richter.

Summary & conclusion

In our opinion, Krka is one of the best companies in Eastern Europe, a leading global player in a growing, non-cyclical sector and can be considered a dividend aristocrat in CEE. The generics segment is highly promising as governments and healthcare institutions in many countries are cutting back on their healthcare expenses and encouraging the use of relatively cheap generic products.

In our view, only a few CEE-based companies have such a history of earnings and dividend growth as Krka. Since its IPO, the company’s market capitalization has increased 18 times. As negatives, we consider the significant share of revenues from the CIS region (especially Russia) as well as the low share ownership of the company’s Management and Supervisory Board, which at the end of December 2021 equalled 0.12%.

While Krka seems fairly valued at present – its current EV/EBITDA 2023E multiple equals 5.8x compared to a 6y average of 5.9x – its stock is highly interesting in the long run, in our view. Currently, the dividend yield for 2022E and 2023E equals 5.9% and 6.4% respectively. The company has a long-term dividend policy, which foresees the payout of min. 50% of its net profit.