We are a leading, management-owned research boutique with a focus on companies from Europe. Our role is that of an intermediary between companies on the one hand and investors on the other.

Our research products are directly distributed to more than 200 mutual and pension funds, family offices and independent asset managers from Central and Eastern Europe, the German-speaking region, Scandinavia, France and UK. In addition, we publish our reports on platforms such as Thomson Reuters, Capital IQ, Factset, Researchpool.com, rsrchxchange.com, ERI-C.com, Visiblealpha.com, ISBNews and PAP, thus ensuring that they are available to institutions from around the world. By organising roadshows and conferences, we provide investors with direct access to corporate decision makers.

Our team consists of professionals with long capital market experience in both Western Europe and the CEE region.

Team

Adrian Kowollik

Adrian Kowollik is Managing Partner at East Value Research and the analyst covering the sectors Technology/Media/Telecom, IT, E-Commerce and Health Care. He graduated in Business Administration from Humboldt University in Berlin and has more than 8 years of experience in equity research and corporate finance. Adrian, who grew up in both Poland and Germany, is a strong believer in the concept of broker-independent equity research and the advantages, which it provides to both companies and investors. Linkedin profile

Mateusz Pudlo (Analyst)

Mateusz Pudlo is Analyst. He has a Bachelors‘s degree in Accounting and Finance from the Wroclaw Business School and a Master’s degree in Economics and Business from Erasmus School of Economics in Rotterdam. His tasks include the preparation of sector reports, company analyses and valuations. Previously, he worked as Assistant in Accounting at EY (Polish branch).

Yusuf Bilgic (Advisor)

Yusuf Bilgic is Advisor to East Value Research. During his impressive career, he was among others Managing Director, Head of Equity Sales & Equity Sales Trading at Lampe Capital in London (previously, part of the German Oetker Group); Director Equity Sales at the oldest German private bank Bankhaus Metzler in Frankfurt; and Vice President Cash Equity Sales Trading at Banco Santander in Frankfurt. Among his clients were institutional investors incl. long/short hedge funds from continental Europe, UK and the United Arab Emirates. Yusuf is based in London.

Michael Lexa (Advisor)

Michael Lexa is Advisor to East Value Research. He looks back at a successful career as Equity Sales among others at Centrobanca, Julius Baer and Dresdner Bank. Over the last 30 years, Michael, who is based in Milan, has been introducing Italian listed companies to DACH-based institutional investors.

Services

Research

We provide broker-independent research on companies that are headquartered in Europe. Our main focus is on small-, micro- and nanocaps, an area, which is usually below the radar of typical brokerage houses. Scientific studies have shown that broker-independent research can be very helpful for companies when it comes to increasing their market visibility and liquidity.

In addition to analysis of single companies, which can be either sponsored or fully independent, we also offer sector reports, whereby we leverage our sector expertise and knowledge of markets in Western and Eastern Europe. Investors can gain access to all our past and future research reports through 1. the relevant research platforms and 2. by purchasing a yearly subscription on our website.

Roadshows

For the companies, which we cover, we organise international roadshows. Thus, we provide them with access to new investor groups and help to diversify the shareholder structure. Through our broker partners, we can also act as an intermediary in capital market transactions.

Consulting for Start-ups

In addition to services for listed companies, we also offer advisory for European start-ups, especially when it comes to raising capital in CEE and Western markets.

Valuation Services & Corporate Finance

Our offering is complemented by valuation services as well as corporate finance advisory, which we are able to offer our clients through our partnership with the Berlin-based firm InveSP Capital Partners. InveSP Capital Partners provides M&A, restructuring and financing advisory services for smaller companies from Western and Eastern Europe. In the last years, it has completed transactions worth EUR >1bn, many of which were crossborder deals.

Imprint

East Value Research GmbH Gontardstr. 11 10178 Berlin Germany Tel.: +49 30 20609082

E-Mail: kontakt@eastvalueresearch.com Represented by: Adrian Kowollik Commercial Register: Registration at Amtsgericht (District Court) Berlin-Charlottenburg under the registration number HRB 164473 B. VAT-Id: DE298268078

Copyrights All rights reserved. Reproduction, commercial redistribution and entry into commercial databases are only allowed with the written consent of East Value Research GmbH.

Liability This website www.eastvalueresearch.com has been prepared with the greatest possible care. However, East Value Research GmbH cannot guarantee that the information contained herein is correct or precise. Any liability for damages, which result directly or indirectly from the use of this website, will not be assumed if it is not intentional or reckless. If there are links to external websites, East Value Research GmbH will not take the responsibility for their content.

Conflicts of interest East Value Research GmbH has taken several measures to prevent conflicts of interest. One of these is that its employees are prohibited to trade in stocks from its coverage that is being sponsored e.g. by issuers. In addition, its employees are not permitted to accept gifts or any other beneficial contributions from individuals, who have an interest in the content of our research publications.

NewConnect was launched on 30 August 2007 as an alternative market of the Warsaw Stock Exchange for young, innovative companies with high growth potential. From the start, it was intended to offer young companies an easy and inexpensive way to become publicly traded. In its early years, the NewConnect segment grew rapidly — in a record-breaking 2011, 172 companies made their debut. After several scandals that caused significant losses for investors, the market is currently undergoing revitalization, including segmentation such as NC Focus for high-quality companies and simplification of information procedures.

Sources: Google search, East Value Research

Current market statistics

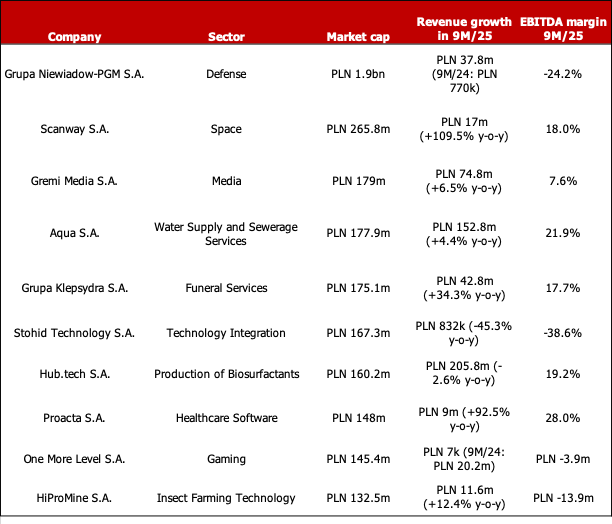

Currently, the website www.newconnect.pl lists 356 companies from various sectors, thereof 5 foreign ones. Their total market capitalisation equals PLN 13.3bn. On December 9, trading turnover equalled PLN 5m/EUR 1.18m, with Sygnis S.A. (PLN 467k, Sector: Additive production technologies), Scanway S.A. (PLN 381k, Sector: Space) and Grupa Niewiadow-PGM (PLN 401k, Sector: Defense) being the most traded stocks. In Q3/25, the total trading turnover amounted to PLN 672.7m/EUR 159m.

Below is a list of the 10 largest NewConnect companies by market cap:

Sources: stooq.pl, bankier.pl, company websites, East Value Research GmbH

Success stories and controversies

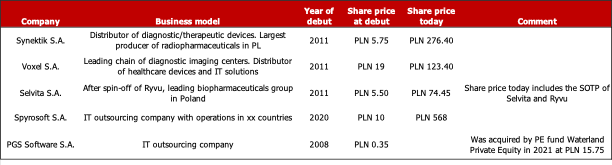

There are a number of companies that debuted on the NewConnect segment—often to raise equity capital for growth because the VC sector is underdeveloped in Poland—over the years grew their business and valuation significantly, and finally moved to the regulated main market of the Warsaw Stock Exchange. Examples include Synektik S.A., a distributor of diagnostic and therapeutic devices and producer of radiopharmaceuticals; Voxel S.A., the leading operator of diagnostic imaging centers in Poland and distributor of medical devices and IT solutions; Spyrosoft S.A., an IT outsourcing company with operations in 10 countries on 4 continents; Selvita S.A., which today — after the spin-off of Ryvu Therapeutics — is the leading Polish biotechnology group; and PGS Software S.A., another IT outsourcing company, which in 2021 was aquired by a Dutch private equity group.

Sources: Google search, East Value Research GmbH

On the other hand, there are also multiple examples of NewConnect-listed companies that do not meet basic corporate governance standards, delay the release of financial reports, and have very low daily trading volume, which makes it difficult to buy or sell larger positions. In recent years, the Warsaw Stock Exchange has put stronger focus on eliminating these pathologies.

Recommendation for investors

Although they can generate significant returns for shareholders, we believe that investments in the NewConnect segment require a very profound due diligence of the company’s business models, their management teams and shareholders. We recommend to commit only a small fraction of the portfolio value to these companies.

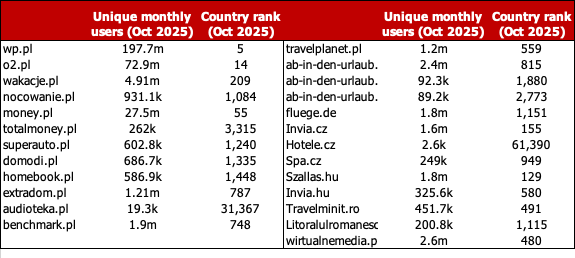

Owned by three members of its management board, who still control >50% of the votes, Wirtualna Polska Holding (WPL) is the largest Polish operator of online portals. Among its websites, there are wp.pl and o2.pl, the 2ndand 4th most popular online information portals in Poland, money.pl (No 1 financial portal in Poland), WP Sportowe Fakty (online sports service), pudelek.pl (No 1 entertainment portal), wakacje.pl (No 1 travel search engine), among others. Wirtualna Polska also operates the digital TV channel WP (available on the 8th multiplex (MUX8), on Cyfrowy Polsat and CANAL+ satellite platforms, in selected Polish cable networks and the Pilot WP service) and radio Open.fm (most popular internet radio in Poland). Since December 2024, the company has also been a strong international player in travel due to its acquisition of 100% of the Czech Invia Group for c. EUR 244m, which apart from Czechia is active in Germany (operates the popular travel search engine ab-in-den-urlaub.de there), Austria, Switzerland, Slovakia, Hungary and Poland. Wirtualna Polska Holding currently has >2,000 employees and has been listed on the Warsaw Stock Exchange since 2015, when it debuted at an IPO price of PLN 32. Apart from 2020, the company has been a regular dividend payer, with its dividend policy foreseeing a DPS of PLN >1/year and a target payout ratio of max. 70%.

Below is an overview over the latest traffic statistics of its web portals:

Source: similarweb.com, East Value Research GmbH

Financials

Since 2014, Wirtualna Polska has demonstrated rapid growth, with revenues increasing at a CAGR of 22.8% to PLN 1.57bn in 2024 and EBITDA rising at a CAGR of 25.9% to PLN 446.8m. Between 2022 and 2024, the company recorded an average gross margin of 65.8% and an average ROCE of 14.2%. Following the acquisition of Invia Group — which, according to Wirtualna Polska, generated annual revenues of EUR 183m and adjusted EBITDA of EUR 37m in 2024 — WPL’s revenues reached PLN 912.8m in H1 2025 (+24.9% y/y). Adjusted EBITDA amounted to PLN 207.7m (+13.7% y-o-y, with a margin of 22.8%), while net income declined to PLN 3.2m (-91.7% y-o-y).

The sharp drop in profitability y-o-y was mainly driven by a 46.2% increase in external service costs (including, for instance, marketing and IT services), PLN 12.7m higher interest expenses, and a 34.7% increase in depreciation and amortization following the Invia acquisition in Q4/24.

Regarding business segments, Tourism has become the most significant for WPL, accounting for 48.7% of total revenues and 37.5% of total adjusted EBITDA in H1/25. Other key segments include Advertising (35.6% of revenues and 53.5% of adjusted EBITDA) — the most profitable segment, with an EBITDA margin of 34.1%— and Consumer Finance (12.8% of revenues and 7.5% of adjusted EBITDA). Thus, the group’s overall performance is dependent on the economic cycle.

As the Invia acquisition was financed with debt, WPL’s net debt increased to PLN 1.26bn after H1/25, up from PLN 482.6m at year-end 2024. Although net gearing of 140.5% is high, the structure of interest-bearing debt is favorable, with 94.8% being long-term. In H1/25, WPL generated solid net operating cash flow, up 20.7% y-o-y to PLN 297m.

Summary & Conclusion

Over the past 12 months, WPL’s share price has declined by 28%, significantly underperforming its benchmark index, the mWIG40, which delivered a 32.6% return over the same period.

Although WP’s share price currently trades below its 200-day moving average, the stock appears to present an attractive long-term investment opportunity. WPL is management-controlled, has a strong brand, an excellent track record, and ranks among the largest listed online groups in Central and Eastern Europe. The group has consistently generated EBITDA margins above 20%, and current sell-side consensus estimates for its EPS growth in 2026E and 2027E of 127.8% and 17.5%, respectively, stand well above the corresponding P/E ratios of 8.2x and 7.0x.

In terms of market potential, both advertising and travel spending in Central and Eastern Europe still offer significant growth opportunities compared with Western Europe. For instance, in Poland, advertising spend per capita remains roughly 3.5 times lower than in Germany, while household spending on travel in Poland, Hungary, Czechia, and Slovakia represents only 3–4% of total expenditures, compared to 6.1% in Germany.

This blog post is the result of our recent trip to Hungary, which amazed us with its rich historical heritage, cleanliness, and excellent transport infrastructure.

Like Poland, the modern Hungarian state emerged after World War I, following more than 370 years of foreign rule — primarily under the Ottoman and Habsburg empires. During most of World War II, Hungary collaborated with Nazi Germany, in contrast to Poland, whose underground army bravely resisted the occupiers. After 1945, both Poland and Hungary became communist countries and members of the Warsaw Pact. However, Hungary followed a more liberal path: its Communist Party allowed, for example, small private businesses, limited company-level decision-making on production and pricing, and travel to the West. As a result, by 1990, when the Soviet bloc collapsed, Hungary’s GDP per capita was more than 100% higher than Poland’s (USD 3,312 vs. USD 1,629).

However, over the last 35 years, Poland has developed more successfully than Hungary, largely due to the bold economic reforms implemented by Finance Minister Leszek Balcerowicz in the early 1990s. In contrast, especially since 2010, when Viktor Orbán’s Fidesz party first gained an absolute parliamentary majority, Hungary’s macroeconomy has developed weaker and the country-which like Poland joined the EU in 2004-has faced significant international criticism—not only from the EU but also from global investors. The reasons include controversial reforms such as the nationalization of private pension assets, the alleged weakening of courts, the centralisation of media ownership close to the ruling party, and the rejection of several important EU initiatives e.g. on sanctions against Russia.

Poland vs. Hungary: Average GDP growth and nominal salary growth, current inflation rate, government deficit, public debt as % of GDP and unemployment

Sources: Polish Statistical Office, tradingeconomics.com, East Value Research GmbH

The Hungarian capital market vs. other CEE countries

With 40 listed companies and an annual turnover of c. EUR 9bn, the Hungarian stock exchange is the 2nd most liquid one in CEE – with >2x higher annual turnover than the Czech and >3x the Romanian one – but is far behind the Warsaw Stock Exchange (760 listed companies, c. EUR 175bn yearly turnover). The trading activity in Budapest concentrates on just four names: OTP (Bank), MOL (oil & gas), Richter Gedeon (Pharma) and Magyar Telecom (Telco). Despite a weaker economic performance and less solid public finances, the main Hungarian equity index BUX has outperformed the Polish WIG (both exclude dividends, which in both countries are significant) by a wide margin over the last 10 years (367.5% vs. 109.5%).

What are currently the most interesting stocks in Hungary?

In our opinion, only a handful of stocks on the Budapest Stock Exchange are actually tradeable for international investors.

While bank stocks—especially OTP—are fundamentally strong, we believe their valuations are currently at a peak and are likely to decline as central banks cut interest rates. However, several other companies appear undervalued, offer attractive dividends, and are expected to continue performing well.

The first of our top picks is Richter Gedeon, a vertically integrated specialty pharmaceutical company with global sales, >11,600 employees and a yearly R&D budget that corresponds to 10% of its annual sales. The company’s pipeline of projects includes several dozen projects in the areas of Neuropsychiatry, Biosimilars, Women’s Healthcare and Blood & Metabolism/Cardiology/Pain & Neurology, most of which have already completed or are currently undergoing clinical studies. Richter Gedeon has been paying attractive dividends (current DYield equals 4.8%) each year since 1995 and is currently trading at PEG ratios of just 0.65-0.70 based on analyst’ EPS estimates for 2025E-2026E.

Another company, which we like now, is Magyar Telecom, the largest Telco operator in Hungary and Northern Macedonia that is owned by Deutsche Telekom. Out of 9.6m Hungarians and 1.8m North Macedonians, Magyar Telecom has 6.6m mobile clients, 1.6m broadband, 1.4m Pay TV and 1.2m fixed voice customers. The company, which due to its stable cash flows has been able to pay dividends and conduct buybacks each year since 2020, is currently trading at an EV/EBITDA 2025E of 4.9x (Orange Polska: 5.3x, Hrvatski Telekom: 7x) and a DYield of 4%. Its net gearing equals 47.4% and is thus at a reasonable level.

Finally, our third pick is MOL, which is the Top 3 integrated oil and gas company in all countries of the fast-growing CEE/SEE region. In addition, it has upstream operations in the CIS region incl. Russia (which we consider the main risk), Iraq, Pakistan and Egypt. According to its latest investor presentation, with currently >25,000 employees it explores and produces oil (c. 94,000 of oil equivalents per day), has a capacity of 380,000 barrels per day in currently 3 refineries, operates 2 petrochemical facilities, >2,300 service stations and a 6,000 km natural gas pipeline in Hungary. Its current reserves equal 332,000,000 barrels of oil equivalent. Latest net gearing equals 17.4%, the current EV/EBITDA 2025E is historically low (2.6x vs. a 5-year average of 3x) and the DYield of 9.5% very attractive. In 2025E-2030E, MOL plans to spend 30-40% of its c. USD 1.9bn CAPEX on low-carbon circular projects in the areas of waste management, biogas production, green hydrogen and solar, among others.